Adobe Inc. Financial Outlook & Expectations

Disclaimer: CAG is a registered investment advisor. This analysis is not a personal recommendation to buy or sell Adobe. Not all investments are suitable for all people. Investing involves risk including the potential loss of principal. This analysis is based on consensus analyst expectations & the publicly available information about the stock.

Intro

Adobe Inc. is the software company that produces digital media software like Photoshop, Adobe Premiere, After Effects, & Adobe Acrobat PDF Reader. They have a large catalog of offerings, too many to mention here but those are the most recognizable products. Adobe is in our Quality Model and we are optimistic about the future performance in Adobe if we are correct about the following factors:

1) Adobe will continue to be a leader in the Digital Media space

2) Generative AI will take much longer to create comparable entertainment relative to human generated entertainment

2*) Consumers will still demand human generated content indefinitely

3) Adobe can integrate AI tools to better their existing product line

4) Adobe can maintain strong fundamentals and continue to return value to shareholders through growing free cash flow

5) Consensus estimates are close in their forecast for the next 3 years

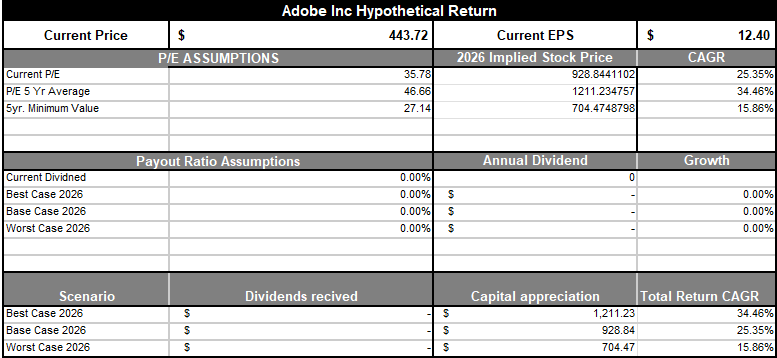

If analyst expectations are met, and Adobe can generate $25.95 in earnings per share in 2027, investors could expect to see greater than market returns by owning Adobe’s stock.

Breakdown of The Business

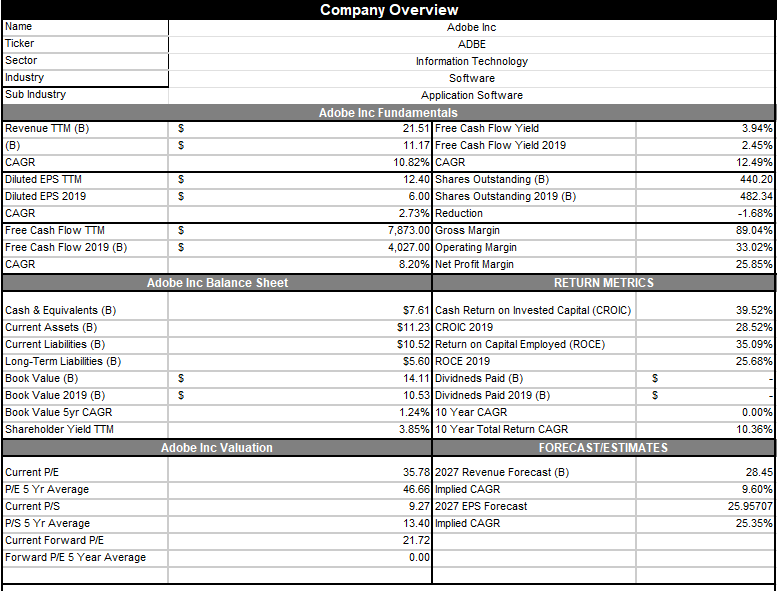

Adobe has been a strong business & a leader in the digital media space throughout the company’s history. They have 3 business segments: Digital Media, Digital Experience, Publishing & Advertising.

Digital Media represents 74% of their annual revenue, this segment encompasses all of their applications, cloud services, document cloud, APIs, integrations, and generative AI assistants. Their largest segment has gross profit margins of 95.71%. Most of this is recurring revenue as well, monthly subscriptions are the driver of this segment. Annualized recurring revenue for the digital media segment, assuming no growth or cancellations of service for 2025, is $17.216B. For 2024 this segment has 15.864B in revenue.

Digital Experience generated 5.366B in revenue with 1.589B in cost of goods sold (COGS), so gross profit margins of 70.38%. Publishing & Advertising generated 0.275B in revenue with 0.089B in COGS, so gross profit margins of 67.63%.

Fundamentals

If we look at the income statement, Adobe has been a fast growing & profitable business. In 2024, they achieved a combined gross profit margin of 89.04% and a net profit margin of 25.85%. Selling, General, & Administrative (SG&A) Expense is their largest expense followed by Research & Development (R&D)

Over the past 10 years, Adobe has grown revenue by 16.19% CAGR and has grown earnings per share by 25.89% CAGR. They have grown free cash flow by 19.88% CAGR and reduced share count by 1.22% CAGR over the past 10 years. These growth numbers have moderated over the past 5 years however, even though they have still grown revenue by double digits and are expected to resume double digit profit growth in the next few years.

If we look at the balance sheet, they have 7.61B in cash as of the end of 2024 and 1.5B in debt coming due in 2025. A large part of their long term assets is Goodwill & Intangibles, which is typically less desirable than tangible assets. They have 13.57B in Goodwill & Intangibles out of 30.23B in Total Assets. Persistently high goodwill can be an indication that Adobe overpays for acquiring other companies, its also an indication of the power of the brand that Adobe has created. Either way, this would only be valuable to Adobe if they were acquired themselves. They cant monetize the goodwill on the balance sheet in the same way they could with fixed assets. With goodwill being 45% of their total assets, that's way higher than a company like Google (7% of total assets), but comparable to a company like Oracle (46% of total assets).

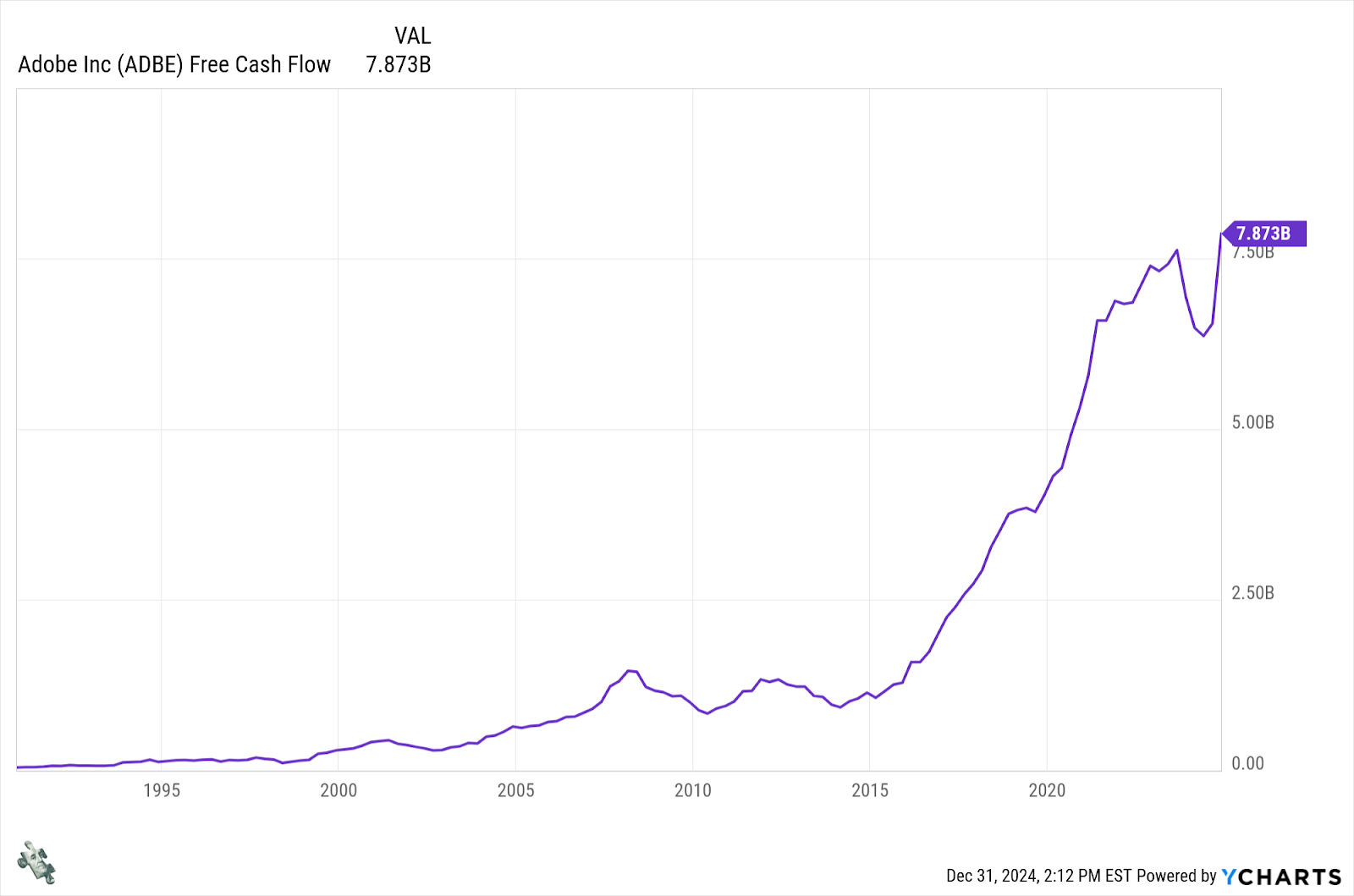

Looking at cash flow, they generated a 8.056B in cash flow from operations, which is way above what is needed to reinvest in the business/service debt/ and continue to buy back shares. They generated 7.87B in free cash flow in the past 12 months.

Valuation & Return Profile

Bear Case: Adobe is currently trading at 35.78x earnings, this is below the 5 year average of 46.66x earnings. This year, Adobe returned -23.29% as investors are concerned that generative AI tools will render Adobe’s business model obsolete. As a generative AI user, but not a generative AI expert, my opinions are not expert opinions. I am of the belief that there is a wide gap between where generative AI tools are now and where they would need to be to render human generated entertainment obsolete. Given the rapid progress of other technologies, I might be understating the potential for exponential progress on the generative AI front. If that is the case, then why pay Adobe for video editing software, when you can just generate a movie by typing the plot into a large-language-model like ChatGPT. The same would be true for photo editing software like Photoshop, which has already integrated AI tools to enhance photo editing. This is a material threat to their existing business model and its being priced into the stock & performance in 2024.

Base Case: Adobe continues to integrate these AI tools to enhance their product line, human generated content is enhanced with these tools but 100% AI generated entertainment is still a long way away or humans favor human generated content despite how good AI entertainment gets. Other segments continue growth in line with consensus expectations. Investors could expect return to average valuations & double digit increases in earnings per share, driving the stock price higher.

Best Case: Adobe is a leader in the generative AI space, developing tools to merge AI tools with human generated content. Improves efficiency & costs for content creators and they maintain their dominance in the space and resume impressive growth trends with high margins. You could see valuation expansion beyond the average PE and impressive growth in earnings per share.

Price Targets:

Bear Case: Price target is tough to quantify, the worst case scenario is their product line becomes obsolete and they would have to pivot & service other demands. You could imagine the stock much lower from where it is right now.

Base Case-> Bull Case: Assuming consensus expectations for the business are correct, the forecasted $25.96 earnings per share estimate in 2027 represents 25.35% growth. If Adobe maintains the current P/E ratio, that would put the 2027 price target for Adobe at $928.84. That represents an average return of 25.35% over the next 3 years. If the P/E ratio expands to the 5 year average P/E of 46.66, that represents a 2027 price target of $1211.23 or a compounded average return of 34.47% over the next 3 years.

What The Market Is Pricing In

Given 1 year expectations for both the growth of Adobe & growth in the overall stock market, the price of Adobe’s stock is indicating a 28% premium on Adobe for their 1 year growth outlook. The consensus growth expectation for the S&P 500 next year is +19.23% according to data provided by S&P Global. Adobe has provided guidance for 2025, they expect to generate $16.10 in earnings per share next year which is +29.83% growth

Given the S&P 500 has a P/E ratio of 27.87, you could extrapolate that Adobe should have a P/E multiple of 43.23 (a 55% premium). Which puts the 2025 price target for Adobe at $696.04 which is 56.9% higher than where it is right now.

There are a lot of assumptions in that math, but from that perspective it appears Adobe is trading at a discount considering management underestimates EPS relative to consensus expectations from analysts covering the stock and Adobe is trading at 35x earnings. Consensus estimates may be overly optimistic on EPS growth for the S&P 500 next year which would also change the output.

Disclaimer: CAG is a registered investment advisor. This analysis is not a personal recommendation to buy or sell Adobe. Not all investments are suitable for all people. Investing involves risk including the potential loss of principal.